Washington, January 29, 2025

An International Monetary Fund mission, led by Magnus Saxegaard, and comprising Christian Bogmans, Shinya Kotera, Yen Mooi, and Jonathan Pampolina conducted discussions for the 2025 Article IV consultation with the Slovak Republic virtually during December 4-13, 2024, and in Bratislava, Slovakia, during January 15-28, 2025. Sumiko Ogawa, Financial Sector Assessment Program (FSAP) mission chief, joined the concluding meeting. At the conclusion of the visit, the mission issued the following statement:

Slovakia, like much of the EU, faces headwinds related to geoeconomic fragmentation, high energy costs, and demographic change. Growth has held up in recent years, but at the cost of a much-increased fiscal deficit. Steadfast implementation of the authorities’ ambitious 4-year consolidation plan is needed to reverse the upward trajectory in public debt, alongside policies to strengthen financial resilience and structural reforms to bolster medium-term growth, including through efforts to strengthen governance and reduce vulnerability to corruption.

Economic Developments, Outlook, and Risks

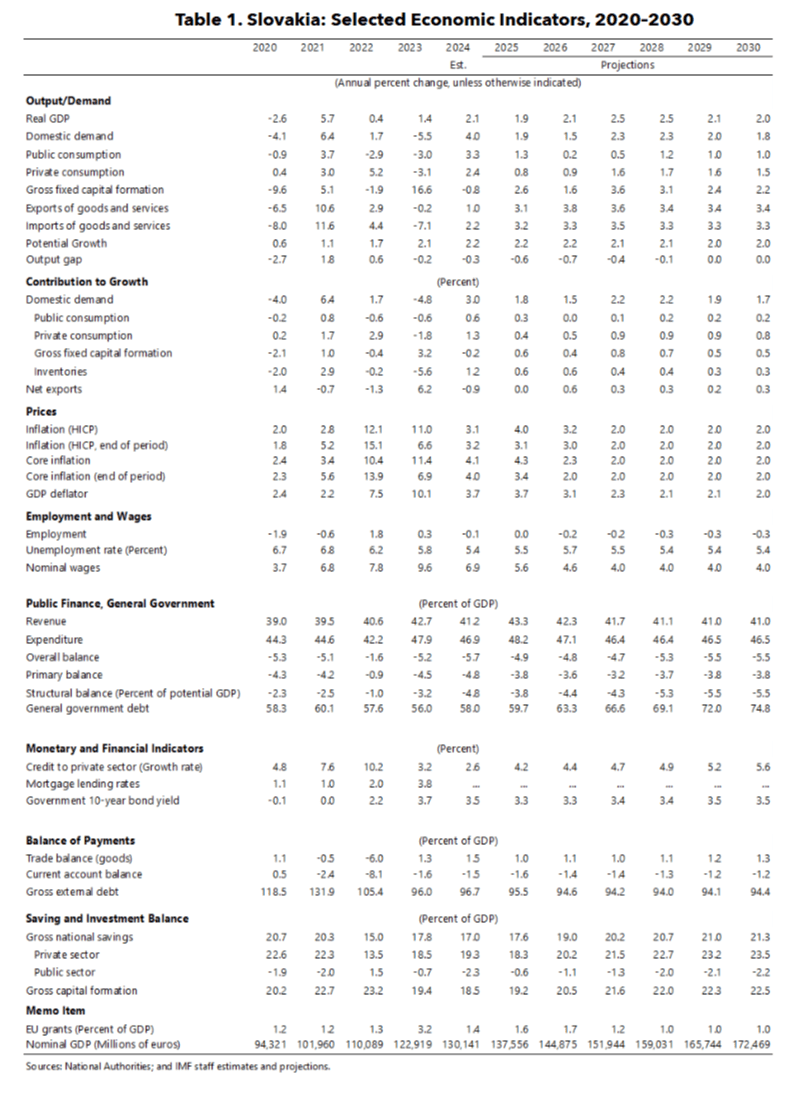

The Slovak economy is recovering. The economy slowed sharply in 2022-23, but growth is estimated to have accelerated to 2.1 percent in 2024, outpacing that in the euro area. Private consumption was the main driver fueled by recovering real wages, the extension of household energy support, and more generous pensions. Meanwhile, an increase in public consumption partially offset a slowdown in EU-funded public investments. While inflation has declined from record-highs in 2023, it increased in 2024H2 due to higher global food price inflation. Core inflation is higher than in the euro area, driven by a tight labor market and strong nominal wage growth.

Economic growth is projected to moderate to 1.9 percent in 2025, before rising to 2.1 percent in 2026. The fiscal consolidation in 2025 will lower growth directly by slowing government spending, and indirectly as higher taxes put upward pressure on prices and dampen private consumption, though the effect will be partially mitigated by the one-year extension of household energy support and strong EU-funded public investments. Meanwhile external demand is expected to remain subdued. For 2026, higher growth in trading partners and increased capacity in the automotive sector is expected to boost exports. Inflation is projected to rise temporarily to 4.0 percent in 2025 and moderate to 3.2 percent in 2026. Adverse demographic trends and lower productivity growth imply that Slovakia’s medium-term growth, as projected by staff, is expected to be significantly lower than its pre-pandemic average, and below IMF forecasts of medium-term growth in other Central, Eastern, and Southeastern Europe (CESEE) countries with comparable income levels.

Risks to growth are tilted to the downside while risks to inflation are broadly balanced. Near term risks include a global slowdown or intensifying trade policy uncertainty which would weigh on growth and exert downward pressure on inflation. Domestically, slippages in fiscal consolidation could increase sovereign spreads and tighten financial conditions. A lack of political consensus on structural reforms and concerns about institutional quality could deter private investment and slow the disbursement of EU funds that have been critical in supporting public investment. A correction in real estate prices combined with an economic downturn could trigger losses for financial institutions. Meanwhile, continued strong nominal wage growth could undermine competitiveness and keep inflation elevated.

Fiscal Policy

Slovakia’s fiscal outlook is challenging. The fiscal deficit is projected to have increased to 5.7 percent in 2024 from 5.2 percent in 2023 due to a combination of revenue easing and higher spending that more than offset the 0.6 percent of GDP in net consolidation measures in the 2024 budget. This increase follows the 3.6 percentage points of GDP widening of the fiscal deficit in 2023. While the change in government in October 2023 meant time to finalize the 2024 budget was short, it is clear ex-post that robust growth combined with significant medium-term fiscal challenges would have warranted a tighter fiscal stance in 2024.

The mission welcomes the authorities’ ambitious fiscal consolidation targets for 2025-28, which is commensurate with the scale of Slovakia’s fiscal challenges.

- The 2025 budget targets a reduction in the headline deficit to 4.7 percent of GDP. Fund staff’s more conservative macroeconomic forecasts imply an overall deficit of 4.9 percent of GDP in 2025. However, the projected structural tightening is broadly in line with the budget. These forecasts are subject to significant downside risks, including from a lower-than-expected yield from the fiscal consolidation measures or a worse economic outlook. If revenues in 2025 appear to be falling short of targets (as implied by staff’s macroeconomic forecasts) the authorities should limit the resulting increase in the deficit, including by saving as much as possible of the contingency buffer.

- Beyond 2025, the medium-term fiscal structural plan targets another 2.5 percentage points of GDP reduction in the fiscal deficit to bring it close to 2 percent of GDP by 2028, though measures to achieve this consolidation are not yet specified. Staff projections suggest that the fiscal consolidation envisaged over the next four years, if met, will reverse the increase in the deficit over the past two years and put public debt on a downward path by the end of the projection period. Staff’s baseline forecast, which does not include any further consolidation beyond that in the 2025 budget, entails a gradual increase in the deficit over the medium term, with public debt rising to 75 percent of GDP by end-2030 from 56 percent of GDP in 2023.

The consolidation measures for 2025 are a step in the right direction. Several of the measures are welcome and will help reduce the deficit on a structural basis, including the increase in the basic VAT rate, and better targeting of child benefits. However, the increase in the number of items subject to reduced VAT rates deprives the government of much needed revenue, while the financial transactions tax (FTT) could weaken financial intermediation and increase incentives for informality.

The measures to lower Slovakia’s fiscal deficit closer to 2 percent of GDP by 2028 should be consistent with Slovakia’s long-term growth and climate objectives, while protecting the most vulnerable in society. While there is no definitive evidence that reducing spending is more effective than increasing revenues in terms of economic efficiency or equity, prioritizing the rationalization of expenditures moving forward would result in a more balanced fiscal consolidation, given the reliance on revenue-based measures thus far.

- Spending: According to Fund staff estimates, value for Money initiatives, including a reduction in subsidies, could yield savings of up to 0.5 percent of GDP, while improved targeting could reduce social spending by as much as 0.8 percent of GDP. Also, there may be scope to increase efficiency by trimming departmental budgets and reducing public sector wage growth, though this should be done cautiously to avoid unintended cuts in service delivery. Reversing the increase of the 13th pension could yield about 0.4 percent of GDP in savings while eliminating the recently introduced early retirement option could yield fiscal savings over the long-term. Finally, energy support measures to households (projected to cost 0.2 percent of GDP in 2025) should be phased out as they are costly and discourage energy conservation.

- Revenues: Reducing the number of items subject to reduced VAT rates could generate as much as 1.3 percent of GDP in savings, while raising property taxes by transitioning to a market value-based system could generate around 0.3 percent in additional revenue. Plans to counter tax evasion and reduce the VAT compliance gap are welcome and could yield up to 0.5 percent of GDP in revenues. Finally, the authorities should replace the FTT with alternative revenue sources, while phasing out the bank levy as planned.

Safeguarding Slovakia’s strong fiscal framework is essential for the credibility of the consolidation effort. Aligning Slovakia’s national expenditure ceiling framework with the new EU fiscal rules avoids inconsistencies and streamlines the budget process but continued focus on the long-term fiscal outlook (beyond the horizon used for the EU fiscal framework) remains useful given Slovakia’s medium-term fiscal challenges. Slovakia’s strong and independent Council for Budgetary Responsibility can help by monitoring the impact of government policies on the long-term sustainability of public finances. Lastly, the mission recommends reforming the debt brake before it comes into effect in 2026, to avoid the risk of a disruptive fiscal consolidation.

The mission welcomes the government’s objective to increase absorption of EU funds. The Slovak government is working with the OECD and the European Commission to identify concrete measures to increase absorption. In this regard, there is a need to strengthen project management capacity, especially at the municipal level, while the preparation of a national investment plan could help guide the timely selection of investment projects.

Financial Sector Policy

The 2024 Financial Sector Assessment Program (FSAP)—an in-depth review of the financial sector—assessed the banking sector to be resilient against severe shocks, reflecting a healthy level of buffers and profitability. The residential real estate market remains a source of vulnerability. In particular, tighter financial conditions, an economic slowdown, and a decline in still-elevated house prices could put pressure on households’ repayment capacity and increase the riskiness of banks’ mortgage portfolios. Also, risks remain elevated in the office segment of the commercial real estate (CRE) market while banks with large exposures to firms facing geopolitical risks could be vulnerable to credit losses. That said, solvency stress tests indicate that banks have sufficient capital to withstand severe macro-financial shocks. Likewise, liquidity stress tests indicate that the banking system as a whole is resilient to funding and market liquidity shocks.

The current macroprudential stance is broadly appropriate, but the policy framework could be further developed over the medium term to help attenuate cyclical and structural risks.

- Residual risks in the residential and CRE markets suggest the current level of the countercyclical capital buffer (CCyB) is appropriate. Borrower-based measures (BBMs) have contributed to contain household credit risk and should remain in force. The authorities should stand ready to activate the systemic risk buffer on banks’ CRE exposures before risks in the sector become systemic.

- The macroprudential policy framework could be further strengthened by adopting a positive neutral countercyclical capital buffer (pnCCyB). A pnCCyB would help safeguard the availability of releasable capital and give policymakers time to collect evidence of a build-up in vulnerabilities. A healthy level of profitability and/or the availability of voluntary buffers would help facilitate a smooth introduction of a pnCCyB. In addition, remaining leakages in the BBMs (e.g. co-financing a mortgage with a consumer loan) should be closed, while the BBM speed limits should be differentiated across borrower categories (e.g. first- and second-time home buyers, investors, and mortgage top-ups).

Financial resilience could be bolstered by strengthening the supervision of less significant institutions (LSIs) as well as the crisis management framework.

- The NBS’s supervisory powers and operational independence should be enhanced by restricting banks’ appeals only to supervisory decisions and corrective measures that are finalized, and by strengthening the legal protections for supervisors. Moreover, the NBS should streamline off-site supervision to align with LSI’s risk profile and strengthen on-site inspections to bolster the overall effectiveness of LSI supervision.

- The financial safety net and crisis management framework should be reinforced by ensuring that the National Resolution Authority (NRA) has adequate resources, preventing the judiciary from suspending or reversing resolution decisions, ensuring NRA resolutions are immediately enforceable, and enhancing the legal protection of staff involved in resolution. Meanwhile, the authorities should remove active bankers from the board of the deposit guarantee fund to prevent conflicts of interest, while expanding the fund’s mandate and financial strength to enable it to play a broader role in crisis management.

Efforts to strengthen the AML/CFT framework should continue. In particular, the authorities should review the criteria for the application of ML/TF sanctions, strengthen coordination between the NBS and Financial Intelligence Unit, and introduce mechanisms to verify beneficial ownership information and sanction the submission of inaccurate information.

Structural Policy

Slovakia needs structural reforms to diversify its economy, enhance resilience to global shocks and sustain productivity growth. The success of the automotive sector has led to decades of strong growth but exposed Slovakia to global trends related to the green transition and automation. To improve resilience and sustain productivity growth the authorities should intensify efforts to promote innovation and technology adoption. In this context, the mission welcomes the increase in direct government R&D spending, but further efforts are needed to stimulate business R&D including in small firms and startups that are not yet profitable. At the same time, deepening the European single market would allow innovative firms to leverage economies of scale. Finally, advancing the capital market union would facilitate cross-border flows of capital including equity financing and venture capital, which is critical for supporting startups, particularly in countries with less-developed capital markets.

The automotive sector is facing headwinds related to the unfolding green transition and rapid rise of electronic vehicle (EV) production in other markets. To address these challenges, the authorities should encourage innovation across the entire domestic EV production supply chain, promote efforts to diversify the economy, and enhance Active Labor Market Policies (ALMPs) to facilitate the movement of workers across sectors.

The challenges of an aging population require policies to increase the labor force. Flexible working arrangements, shortening the 3-year long maximum parental leave period, and improved child and elderly care could increase female participation, while tax credits and restrictions on early retirement could raise labor force participation among the elderly. The recent easing of national visa rules for foreign workers in professions with shortages could boost migrant inflows, but further efforts are needed to integrate and retain migrants, including by scaling up language training and streamlining certification recognition. Increased focus on vocational education and training would help bring down Slovakia’s high youth unemployment.

Maintaining a favorable investment climate, strengthening governance, and reducing vulnerability to corruption will help lift the economy’s growth potential.

- Governance indicators and perceptions of judicial independence lag peers, and recent surveys point to a decline in the perceived effectiveness of anti-corruption policies.

- A new national anti-corruption strategy is expected to be released mid-year. In that context, the authorities should verify that the new institutional framework that replaced the dissolved Special Prosecutor’s Office and National Crime Agency has not weakened the institutional capacity to investigate and prosecute high-level corruption. Also, the asset declaration and conflict of interest framework for high-risk public officials could be improved. Specifically, broadening the scope of covered public officials, and centralizing and digitizing the submission and publication process with robust verification procedures and appropriate sanctions, would be beneficial. Finally, existing safeguards pertaining to the Prosecutor General’s authority to annul decisions by lower-level prosecutors should be strengthened.

- Safeguards to ensure members of the Judicial Council can only be recalled based on specific and reasonable grounds would enhance judicial independence. Also, the crime of “abuse of law”, whereby judges are subject to criminal liability for their decisions, can have an intimidating effect on judges. Additional safeguards to ensure the framework balances the accountability of judges and independent judicial decision-making would be beneficial.

While greenhouse gas emissions have fallen by 50 percent since 1990, further efforts are needed to cut emissions by 55 percent by 2030 and to reach net-zero by 2050. Slovakia should move expeditiously to fully implement the ETS II scheme for road transport and buildings and could consider gradually raising environmental levies in these sectors until the scheme becomes operational in 2027. The authorities should continue exploring options to replace two coal-fired blast furnaces in the steel industry and phase out fossil fuel subsidies. Also, supporting environmental R&D and green technology would support mitigation efforts and economic diversification. Lastly, a more integrated energy market in Europe would encourage investment in renewables and enhance energy security and reduce energy prices.

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF’s Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

The IMF team thanks the authorities and other interlocutors for their generous hospitality and constructive dialogue.

Source – IMF