Paris, 28 November 2024

Also available in: français and español

Generative Artificial Intelligence (GenAI) will impact regional local job markets differently across OECD countries, exacerbating existing urban-rural income and productivity gaps as well as the digital divides between regions, according to a new OECD report.

Job Creation and Local Economic Development 2024 finds that, following a decade of employment growth, over half of OECD regions had reached employment rates above 70% by 2023, with more women joining the workforce, narrowing the gender gap in labour force participation in 84% of OECD regions.

The employment boom has also led to regional labour shortages and gaps, particularly in densely populated urban regions such as Lombardy (Italy) and Hamburg (Germany), as well as in regions struggling with population decline and ageing.

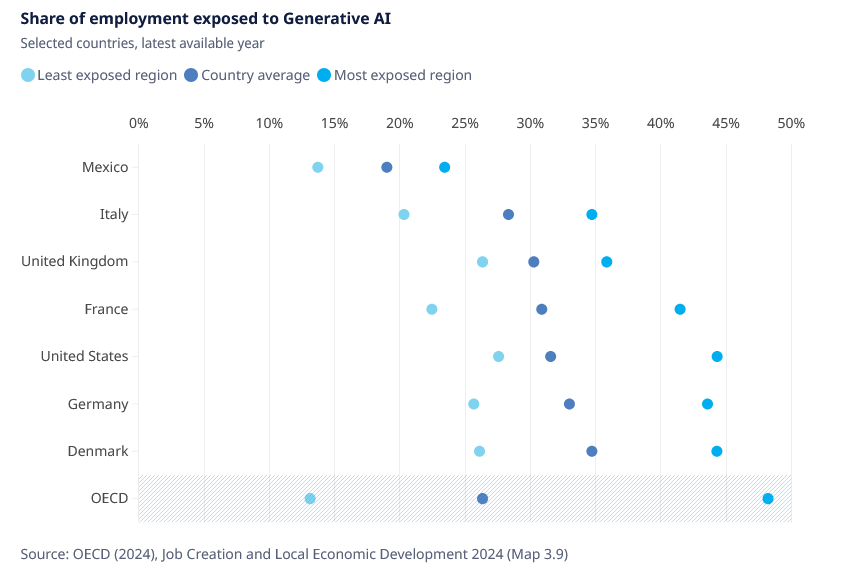

Against this backdrop, Generative AI has the potential to help tackle labour shortages and boost productivity. However, the report highlights significant regional disparities in the extent to which jobs are affected by Generative AI, with the share of workers with jobs exposed to AI ranging from 45% in urban regions such as Stockholm (Sweden) and Prague (Czechia), to 13% in rural regions such as Cauca (Colombia).

Urban workers are more likely to be affected, with an average of 32% already exposed to Generative AI, compared to just 21% of rural workers. This trend could risk worsening existing urban-rural income and productivity gaps, as well as digital divides between regions.

Regions previously considered to be at comparatively low risk of automation are now among the most exposed to Generative AI, according to the report. While technology-led automation has historically affected non-metropolitan and manufacturing regions, now metropolitan areas, high-skilled workers and women face greater exposure as Generative AI excels in performing cognitive and non-routine tasks.

“The rapid adoption of Generative AI is reshaping local job markets, offering solutions to labour shortages and boosting productivity,” OECD Secretary-General Mathias Cormann said. “But it also risks widening the digital divide between urban and rural areas. To harness its potential for all, policymakers must prioritise digital infrastructure, boost digital literacy, and support SMEs to ensure AI’s benefits reach everyone and help tackle local skills bottlenecks.”

The full report Job Creation and Local Economic Development 2024: The Geography of Generative AI along with detailed findings, country notes and graphs is available here:

Abstract

Regions across the OECD face a range of labour market challenges and are undergoing a significant transformation. An ageing workforce, low labour productivity growth, persistent regional disparities, pervasive labour shortages, and new technologies will require both people and places to undergo transitions. This report, Job Creation and Local Economic Development 2024: The Geography of Generative AI, examines the health of regional and local labour markets, including through new estimates on regional labour shortages and their drivers. New tools and technologies, such as Generative AI, could help policymakers address these challenges and seize new opportunities for job creation and local economic growth. This report provides novel evidence of the geography of the impact of Generative AI on jobs across the OECD. It examines which places within countries and types of workers are most exposed to Generative AI and contrasts this with the labour market impact of past waves of technologies that drove automation. Finally, it discusses local and place-based actions and policies for seizing the benefits of Generative AI, such as boosting productivity, mitigating labour shortages and demographic change, as well as for mitigating risks of job displacement.

Executive Summary

Employment rates across OECD regions are at record highs but large disparities remain. In 2023, roughly 3 out of 5 (59%) of OECD regions had employment rates over 70%. Within countries, employment is particularly high in metropolitan regions with a high share of employment in tradeable sectors as well as “younger” labour markets. While the majority of regions have recovered from the COVID-19 pandemic, the recovery was faster and larger in metro regions. Overall, significant disparities persist, with little convergence between top- and bottom-performing regions in critical measures such as employment, labour force participation, and labour productivity. On average, regional employment rates differ by up to 10.5 percentage points in OECD countries.

During this employment boom, gender inequalities in regional labour markets have narrowed but age disparities have widened in most regions, to the detriment of younger workers. The gender gap between men and women in labour force participation has fallen in over four out of five (83%) of OECD regions, with two-thirds of OECD regions recording a fall of more than 1.5 percentage points. In contrast, disparities by age group increased in the majority of regions. The gap in labour force participation between youth (15- to 24-year-olds) and prime-age working population (25- to 64-year-olds) increased in three out of five (almost 60%) of regions, growing significantly by over 1.5 percentage points in half of OECD regions. Young people are struggling more to integrate into the labour market, particularly in metropolitan regions.

A troubling slowdown in labour productivity growth and stark differences among regions persist. Labour productivity growth has remained sluggish over the past decade, with half of OECD regions recording growth of less than 0.8% per year. While the least productive regions grew faster than the most productive ones over the last 10 years, it was not sufficient to result in significant regional convergence. As of 2022, the 20% most productive regions still recorded 50% higher labour productivity levels than the 20% least productive regions in the same country. Overall, labour productivity remains considerably higher in capital regions (one-third higher) and regions specialised in tradable sectors (one-fifth higher) than in the rest of a country.

A diversified skills base aligned with labour market needs boosts resilience; however, OECD regions have recorded a noticeable increase in skills polarisation and struggle with large skills mismatches. On average, the share of middle-skilled jobs fell in four out of five OECD regions over the last decade, in many cases being replaced by high-skilled jobs, but also in some cases low-skilled jobs. Skills mismatches (workers that are either under or overqualified for their jobs) persist and vary widely across regions, with one-third of countries exhibiting regional differences in skills mismatch of more than 10 percentage points between the regions with the highest and lowest skills mismatches.

Labour and skills shortages have become one of the most pressing policy concerns in most OECD regions, not only dynamic urban labour markets. Driven by a combination of both cyclical and structural factors, labour markets have become extremely “tight”, as firms struggle to find suitable workers to fill vacancies at different skill levels. The consequences for both firms and local economies can be significant, holding back firm operations and investments, inhibiting local economic growth, and creating obstacles for seizing new economic opportunities offered by technology or meeting environmental objectives.

Regional labour shortages have risen substantially since 2019 and increasingly affect regions with previously low levels of labour shortages. Labour market tightness (defined as vacancies per employed person) increased significantly (e.g. 50% in Germany, 80% in the U.S.) compared to pre-COVID times (2019-2022). While the severity of labour shortages differs between countries, regional disparities are also significant. Within countries, the tightest regional labour markets report on average five times more vacancies per employed person than the least tight regions. Labour shortages are particularly acute in regions focused on tradable services or high-growth industries.

Many regions face significant labour shortages in jobs crucial for the green and digital transitions. In almost all OECD regions (95%), labour shortages in Information and communication technologies (ICT) are higher than for other jobs, with on average twice as high labour market tightness. Labour shortages are also more pronounced for green jobs in nine out of ten (90%) regions. In European regions, labour shortages are on average more than 40% higher for green-task jobs than for other jobs. The scarcity of green and digital “talent” reflects the adjustment of local economies to the twin transition but could also indicate significant skills mismatches, resulting from structural labour market transformation that has not yet been accompanied by the necessary change in education and training systems adapted to regional workforce needs.

Widespread population ageing risks exacerbating labour shortages, especially in the regions with the oldest age structure. More than four in ten OECD regions experienced a shrinking working-age population over the past decade. If current population trends continued, average regional labour market shortages could increase by almost 9% within the next 20 years, and by nearly 16% in the oldest 20% of OECD regions (rising from one vacancy for every 21 working-age persons to one vacancy for every 18 working-age persons). Policies designed to mitigate labour shortages need to reflect place-specific challenges, such as ageing, retaining and attracting (young) talent to remote regions and facilitating job transitions, taking account of the geographic distribution of jobs.

Generative AI could have a much wider labour market impact than previous technologies that drove automation of tasks, affecting a broader group of people and places. Across the OECD, around a quarter of workers are exposed to Generative AI, meaning 20% (or more) of their job tasks could be done at least 50% faster with the help of Generative AI. Exposure to AI will continue to grow, as new software is developed or integrated with Generative AI technologies, with the share of workers who could be highly exposed (50% of their tasks could be done at least 50% faster with Generative AI) possibly ranging from 16% to more than 70% across OECD regions. In contrast to previous automation technologies, Generative AI excels in doing cognitive, non-routine tasks, shifting regional labour market exposure, with regions concentrating industries such as education, ICT, or finance becoming most exposed to Generative AI.

Regions previously considered to be at comparatively low risk of automation are the most exposed to Generative AI. Technology-led automation, including through other forms of AI, particularly affected non-metropolitan and manufacturing regions. In contrast, Generative AI has the potential to alter a significantly higher share of jobs in metropolitan regions. Exposure to Generative AI is greater for high-skilled workers and women, while previous technology-led automation mainly affected low-skilled workers and men.

While the exact effects of Generative AI on the geography of job creation and displacement remain to be seen, evidence from automation trends show overall net job creation. The share of jobs at high risk of automation, including through forms of AI that predated Generative AI, ranges from around 1% to 29% in OECD regions. However, on average, higher regional risks of automation did not lead to overall reductions in employment over the past decade. Instead, an increase of 10% in the share of jobs at high risk of automation is related to an increase of 5.6% in labour productivity over five years. Yet, in some regions, automation appears to have contributed directly to a loss of overall employment. Moreover, even though new job creation outweighed job losses in most regions, newly created jobs might not have benefitted those workers who lost their jobs due to automation.

New AI technologies could offer a strategic tool for OECD regions to address critical economic and labour market challenges, including labour shortages, and help boost sluggish labour productivity growth. Fostering the adoption of AI technologies could yield a much-needed catalyst for productivity in regional economies. Providing access to AI tools and training can help regions to access untapped talent in low-skilled workers or workers with disabilities for whom many jobs were previously out of reach. In addition, AI technologies can be leveraged to directly supplement workers where feasible, helping to ease labour shortages and the effects of an ageing workforce.

National labour market policies could draw lessons from the uneven recovery from COVID-19 and recent trends in regional labour market performance. By reflecting on the diverse impact and recovery from the pandemic, policy makers could take into consideration the different degrees of resilience to labour market shocks across regions and identify challenges and appropriate policy responses in light of ongoing transformations such as the green-digital twin transition.

In trying to alleviate labour shortages, policy makers need to address their exact, underlying causes, which are often place specific. In some regions, labour shortages might primarily be driven by a lack of available workers, a problem that could be exacerbated by ageing and a shrinking workforce. However, in other contexts, skills mismatches and gaps could be the main driver of labour shortages. Furthermore, some regions struggle with a lack of attractiveness to both attract and retain a skilled workforce. Finally, some regions might rely on employment in jobs that have become less attractive to workers due to lower job quality or work conditions, subsequently creating labour shortages. As such, the right mix of policy responses will need to consider the place-specific factors behind labour shortages.

To seize the opportunities of new technologies and respond to its labour market risks, policy makers could assess regional labour market exposure to different forms of AI. Working with the private sector could foster a better understanding of the job and skills changes that result from the spread of new forms of AI in different regions. This would provide the foundation for more effective up- and re-skilling programmes that are aligned with local labour market needs as well as tailored support for displaced workers. Public-private sector collaboration could help boost the adoption of AI tools, which could raise regional labour productivity, mitigate labour shortages, or offer a new tool to alleviate ageing in regions with significant population decline. Regional policy makers could also consider new opportunities that AI tools could bring such as promoting efficiency gains and enhancing the quality of regional public services or facilitating the labour market inclusion of people with disabilities. Collaboration with social partners to monitor job quality and worker rights should accompany these efforts.

Source – OECD