Paris, 5 March 2025

- Teo Lombardo, Transport Modeller

- Leonardo Paoli, Clean Transport Analyst

- Araceli Fernandez Pales, Head of Technology Innovation Unit

- Timur Gül, Chief Energy Technology Officer

Battery deployment continues to break records as prices fall

The global battery market is advancing rapidly as demand rises sharply and prices continue to decline. In 2024, as electric car sales rose by 25% to 17 million, annual battery demand surpassed 1 terawatt-hour (TWh) – a historic milestone. At the same time, the average price of a battery pack for a battery electric car dropped below USD 100 per kilowatt-hour, commonly thought of as a key threshold for competing on cost with conventional models.

Cheaper battery minerals have been an important driver. Lithium prices, in particular, have dropped by more than 85% from their peak in 2022. However, rapid advancements in the battery industry itself are also supporting price declines. After years of investments, global battery manufacturing capacity reached 3 TWh in 2024, and the next five years could see another tripling of production capacity if all announced projects are built.

These trends point to a battery industry entering a new phase of its development. While markets used to be regionalised and small, they are now global and very large, and a range of technological approaches is giving way to standardisation. Looking ahead, economies of scale, partnerships along the supply chain, manufacturing efficiency, and the capacity to bring innovations swiftly to market will be crucial to compete. This will likely result in greater consolidation across the sector, which is simultaneously being reshaped by government-driven efforts to geographically diversify battery supply chains.

China is set to remain the top producer, but consolidation could transform the market

Today, China produces over three-quarters of batteries sold globally, and in 2024 average prices dropped faster there than anywhere else in the world, falling by nearly 30%. Batteries in China were reported to be cheaper than in Europe and North America by over 30% and 20%, respectively. Declining battery prices in recent years are a major reason why many electric vehicles (EVs) in China are now cheaper than their conventional counterparts.

The price advantage of Chinese producers can be ascribed to four main factors:

- Over 70% of all EV batteries ever manufactured were produced in China, creating extensive manufacturing know-how. This has supported the rise of giant manufacturers such as CATL and BYD, which have centralised expertise in the battery sector and driven innovation. These companies have scaled up production faster and more efficiently than competitors and, crucially, achieved higher manufacturing yields.

- Supply chain integration, as the result of acquisitions by a single company as well as close cooperation among leading firms, has also supported faster innovation and a decline in manufacturing costs, with the latter additionally reported to be supported by access to below-market prices for critical minerals. The Chinese battery ecosystem covers all steps of the supply chain, from mineral mining and refining to the production of battery manufacturing equipment, precursors and other components, as well as the final production of batteries and EVs.

- Chinese producers have prioritised lithium-iron phosphate (LFP), a cheaper battery chemistry. Initially thought to be unsuitable for electric cars due to their lower energy density, years of research and development by Chinese producers have honed LFP batteries, which now cover nearly half the global EV market after more than tripling their share within the past five years. Today, they are about 30% less expensive than their main competitor, lithium nickel cobalt manganese oxide (NMC) batteries, while still offering competitive ranges for EVs.

- Fierce domestic competition has shaped the Chinese battery market, which is home to almost 100 producers. To maintain or gain market share, these firms have been cutting their profit margins to sell batteries at lower prices.

However, price declines could slow in the near future. Amid tough competition and shrinking margins, the number of companies producing batteries in China is likely to fall, and certain producers will acquire greater influence and pricing power. Even so, China is expected to remain the largest battery manufacturer by some distance in the medium-term.

Share of electric vehicle sales by battery chemistry in selected regions, 2022-2024

Battery production in Europe is going through a make-or-break moment

Elsewhere, the competitive edge of China’s electric car and battery industry is presenting major challenges. Many battery producers in Europe are postponing or cancelling expansion plans because of uncertainty about future profitability. Production costs in the region are about 50% higher than in China; meanwhile, the battery supply chain ecosystem is still relatively weak and a lack of specialised workers persists. The bankruptcy of Northvolt – Europe’s largest investment in a homegrown battery maker – underscores the difficulties of competing with Asian producers, with smaller manufacturers struggling to scale up production and reach sufficient yields.

Despite the challenges at hand, there are pathways for building a more competitive battery industry in Europe. All start with ensuring strong domestic demand, which gives manufacturers time to hone production processes and develop strong regional industrial ecosystems. On this front, clear policy that signals continued demand growth and reduces investment risks is essential.

Efforts to produce cheaper LFP batteries in the region are beginning to expand. Over the past two years, Korean manufacturers – traditionally the largest battery manufacturers in Europe – have lost almost one quarter of their market share in the European Union, which dropped from nearly 80% in 2022 to 60% in 2024 in part due to the increased success of LFP batteries made in China. However, some Korean companies have started investing in making LFP batteries in Europe, positioning themselves to better compete with Chinese producers.

In the meantime, Chinese battery makers are likely to keep expanding their European footprint, including through partnerships. Projects such the joint venture between Stellantis and CATL could speed up the uptake of LFP batteries in the region, improve Europe’s battery ecosystem and potentially reduce the cost gap with China.

Share of electric car battery sales by manufacturer’s domicile, 2022-2024

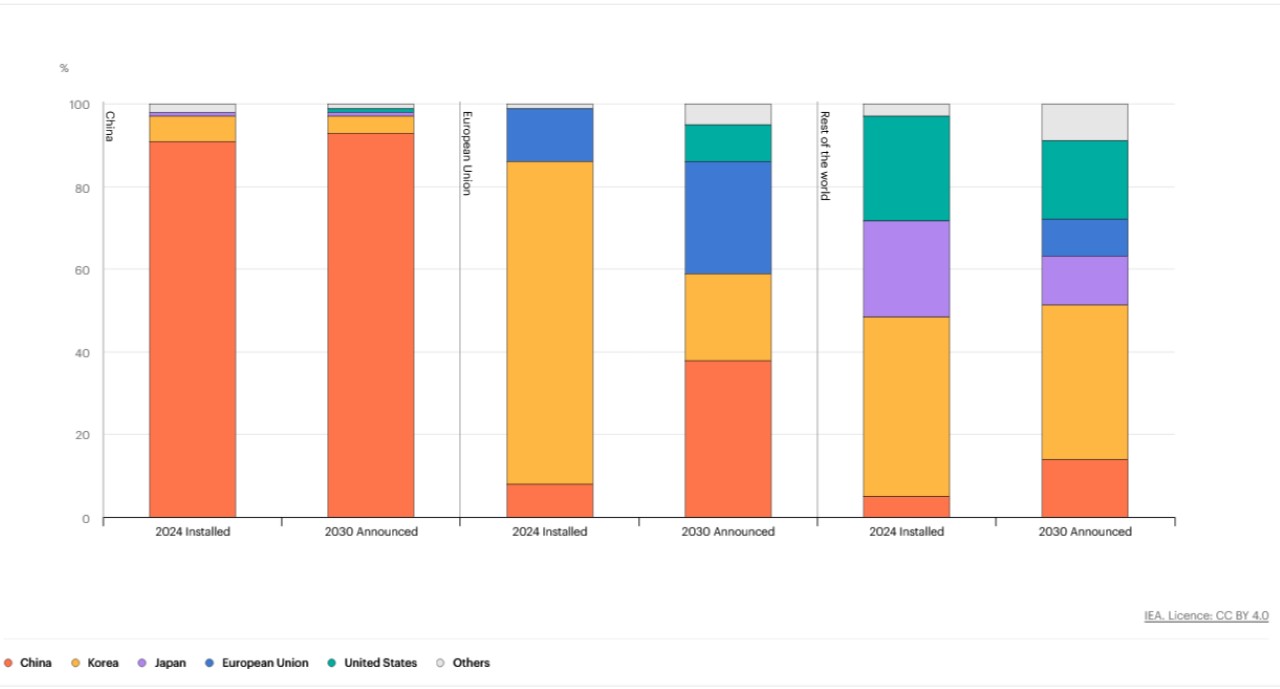

Though China leads, countries worldwide are racing to expand battery production

Despite China’s current market dominance, the expansion of battery production is also moving fast elsewhere.

Korea and Japan are already major players in the global battery industry, home to key battery makers and specialised suppliers with strong expertise in NMC batteries. Both countries have limited domestic battery production but host established manufacturers with significant overseas investments. Korean companies lead in overseas manufacturing capacity, with nearly 400 gigawatt-hours (GWh), far surpassing Japan’s 60 GWh and China’s 30 GWh. Korean producers supplied over one-fifth of global electric car battery demand in 2024, while Japanese producers covered nearly 7%. As their overseas investments grow in major automotive markets, a key question is the extent to which they will embrace cheaper LFP designs. These producers also have strong innovation track records and are among those in the race to develop new technologies such as solid-state batteries.

In the United States, battery manufacturing capacity has doubled since 2022 following the implementation of tax credits for producers, reaching over 200 GWh in 2024. Nearly 700 GWh of additional manufacturing capacity is under construction. Around 40% of existing capacity is operated or developed by established battery makers in close collaboration with automakers. Developing domestic capacity for manufacturing battery components has progressed more slowly, so most anode and cathode demand is still satisfied by imports. Battery demand for stationary applications has increased by over 60% annually for the past two years, opening up a demand stream beyond EVs, albeit smaller in volume.

In the meantime, Southeast Asia and Morocco are emerging as potential production hubs for batteries and their components. Southeast Asia has attracted significant Chinese investment, which could speed up technology and innovation transfer. In Indonesia, home to half the world’s mined nickel, the first EV battery manufacturing and graphite anode plants began production in 2024. Meanwhile, Morocco has the largest reserves of phosphate, a mineral essential for LFP batteries, as well as an established car manufacturing industry and free trade agreements with the European Union and the United States. These factors contributed to over USD 15 billion in announced investments in battery and components manufacturing in 2022.

Share of manufacturing capacity by battery producer’s domicile, 2024-2030

Building a resilient battery industry while remaining competitive is difficult and may require trade-offs

Despite the rapid decrease in battery prices and continued innovation, the degree of concentration in battery supply chains has raised security concerns among governments in recent years. Announcements such as China’s recently proposed export limitations on battery cathode and lithium processing technologies have amplified attention on this issue.

However, diversifying the production of batteries and their supply chain is a substantial undertaking and may require trade-offs. Any country interested in expanding output needs time and investment to bolster domestic manufacturing, build up their expertise and reduce production cost gaps relative to China. Such efforts require sufficient and sustained battery demand, and electric vehicle sales – which today account for 85% of the battery market – are the only driver that can create sufficient volume.

Strategically deploying automation, digitalisation and innovation also has an important role to play in reaching sufficient production yields to compete with Chinese production and facilitate the diversification of supplies. Meanwhile, collaboration with incumbent battery producers, through joint ventures or technology licensing agreements, can decrease the time and investments required to onshore battery production and develop domestic supply chains.

Another key lever is international collaboration. Many individual markets might not be sufficiently large to justify the necessary investments in the manufacturing of batteries and their components, and so may require closer collaboration with other EV and battery markets, as well as cooperation with resource-rich countries such as those in South America and Africa, Australia, Indonesia, to make the case.

The IEA will continue to monitor these trends in order to provide timely analysis and policy advice. Later this year, the Agency will also publish a special report focused on the car industry, which will include new analysis on battery supply chains.

Source – IEA