Washington DC, September 18, 2024

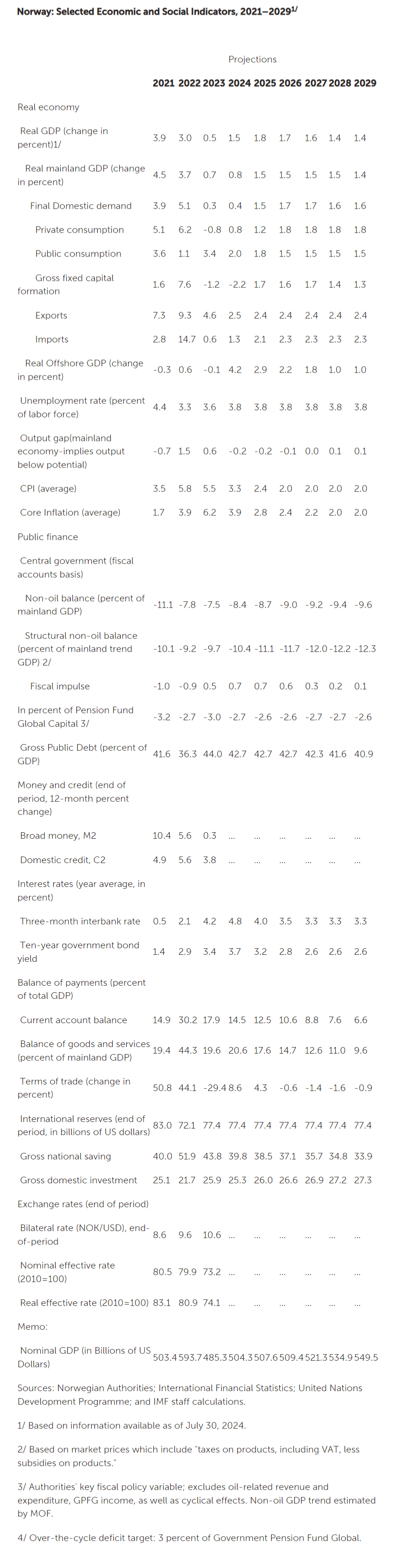

The Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation[1] with Norway. Real GDP growth slowed to 0.5 percent in 2023 from a cyclical peak of 3.5 percent on average over 2021–22. Private consumption and gross fixed investment, particularly residential investment, declined amid tighter financial conditions, with exports and public spending providing some support.

The tighter financial conditions have also impacted the commercial real estate (CRE) sector amid rising debt-servicing costs and declining valuations. While retreating from its 2022 multiyear peak, headline inflation remains high and above the 2 percent target, with persistent services inflation keeping core inflation elevated. The weaker currency has also contributed to keeping inflation high, while inflation expectations remain above the inflation target. The fiscal policy stance is expansionary. Although easing since early 2024, financial conditions remain tight, reflecting a restrictive monetary policy stance following Norges Bank’s cumulative 450 bps increase in its policy rate. Macroprudential policy settings have been tightened across several dimensions over the past two years, and systemic risks are not building up further. The financial system is sound, and bank buffers are robust but vulnerabilities remain high.

Economic activity is projected to rebound in 2024, and real GDP growth would rise to 1.5 percent, supported by a stronger offshore sector, while mainland activity would remain subdued and would rise by 0.8 percent, amid still tight financial conditions. Inflation is projected to reach 3.3 percent by end-2024 and return to the target by mid-2026. Amidst still high uncertainty, risks to the growth and inflation outlook are balanced.

Executive Board Assessment[2]

Directors agreed with the thrust of the staff appraisal. They welcomed the expected rebound in growth, noting that risks to the outlook are broadly balanced. Directors highlighted the need to carefully navigate policy trade-offs arising from elevated inflation and financial sector vulnerabilities. They underscored the importance of comprehensive structural reforms to address the challenges posed by population ageing, productivity slowdown, and geoeconomic fragmentation.

Directors underscored the need to maintain a tight monetary policy stance to ensure that inflation converges to target and to mitigate risks of a de-anchoring of inflation expectations. They encouraged the authorities to continue to employ a data-dependent approach, remaining ready to adjust the monetary policy stance as needed.

Directors welcomed that the financial system is stable, with robust buffers. Noting elevated systemic risks, Directors agreed that macroprudential policy settings should remain tight and recommended continued close monitoring. Elevated household indebtedness and high exposure to commercial real estate (CRE) underscored the need for continued prudent policies. Directors encouraged further progress on the implementation of 2020 FSAP recommendations and welcomed the strengthening of the Financial Stability Authority (Finanstilsynet).

Directors recommended adopting a neutral fiscal stance, highlighting that removing the current fiscal stimulus would support disinflation. They emphasized that discretionary fiscal stimulus should be well-targeted and temporary and deployed only if needed. Directors encouraged efforts to address the increased reliance on natural resource revenues and to adopt measures to ensure that higher defense and ageing-related spending needs can be accommodated. Important measures include increasing the efficiency of the tax system, restructuring the pension and social protection regimes, and complementing the fiscal policy framework with enhanced medium-term budgeting and an expenditure rule.

Directors underscore that comprehensive reforms are needed to foster diversification, raise productivity growth, and mitigate the impact of geoeconomic fragmentation. They emphasized that reforming the sickness and disability benefits systems would help to bolster labor supply. Directors welcomed the authorities’ commitment to enhancing climate mitigation and adaptation.

IMF data on Norway

[1] Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country’s economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis for discussion by the Executive Board.

[2] At the conclusion of the discussion, the Managing Director, as Chairman of the Board, summarizes the views of Executive Directors, and this summary is transmitted to the country’s authorities. An explanation of any qualifiers used in summing ups can be found here: http://www.IMF.org/external/np/sec/misc/qualifiers.htm.

Source – IMF