Brussels, 15 October 2024

Written by Pieter Baert.

For her second mandate, European Commission President-elect Ursula von der Leyen has prioritised strengthening EU competitiveness and simplifying existing EU legislation. One focus here is the regulatory burden in taxation within the EU and its potential evolution. On 17 October 2024, the European Parliament’s Subcommittee on Tax Matters (FISC) is due to hold a public hearing on simplicity and transparency in tax policy.

Making Europe faster and simpler

Mario Draghi’s report on EU competitiveness delivered a stark message: the European economy is facing ‘an existential challenge’. Without decisive action to boost sustainable growth, the EU risks falling (further) behind its competitors, leading Europe down a path where it is poorer, less free and less innovative. While there are multiple reasons for the EU’s slower economic and productivity growth, Draghi’s report (as well as Enrico Letta’s report on the single market) point the finger at the heavy regulatory burden that companies face within the European Union. For instance, while the US Congress has enacted close to 3 500 laws and voted 2 000 resolutions in the past 5 years, the EU has passed approximately 13 000 legislative acts.

At the start of her new mandate, von der Leyen has pledged to address this issue and make the EU business environment faster and simpler. Therefore, each incoming Commissioner will be tasked with stress testing the entire EU rulebook to identify and eliminate overlaps and contradictions. The overall target is to cut the reporting burden by at least 25 %, and at least by 35 % for small and medium-sized enterprises (SMEs). Additionally, all new legislative proposals will undergo a new ‘SME and competitiveness check’ to prevent unnecessary compliance burdens. A Commissioner dedicated to Implementation and Simplification (Valdis Dombrovskis is Commissioner-designate for this portfolio) will assume a pivotal role in coordinating these efforts, presenting annual plans for fitness checks of existing legislation, and conducting ‘reality checks’ with stakeholders to identify any hurdles they face in implementing EU law.

Tax compliance costs

A challenge when considering the issue of compliance costs in the area of taxation is determining which components to include and how to measure them. Various elements may be considered, including staff salaries in a company’s tax department, time spent preparing, collecting and reviewing the required data entries, purchase of tax compliance software, and staff training to use these tools effectively, etc. Costs can multiply when legislation is frequently changed or overly complex, potentially leading to mistakes, audits, penalties, legal fees or even court cases. Ultimately, tax compliance costs impose an additional financial burden on companies that accumulates on top of the tax liability itself, diverting time and resources from other investment opportunities. Companies may also decide not to make certain sales or investments if they consider the associated compliance costs too burdensome.

Less frequently discussed are the costs incurred by tax authorities as a result of new legislation. Complex or poorly targeted tax laws can also strain the personnel or information technology resources of national tax authorities, potentially diverting focus from other essential tasks.

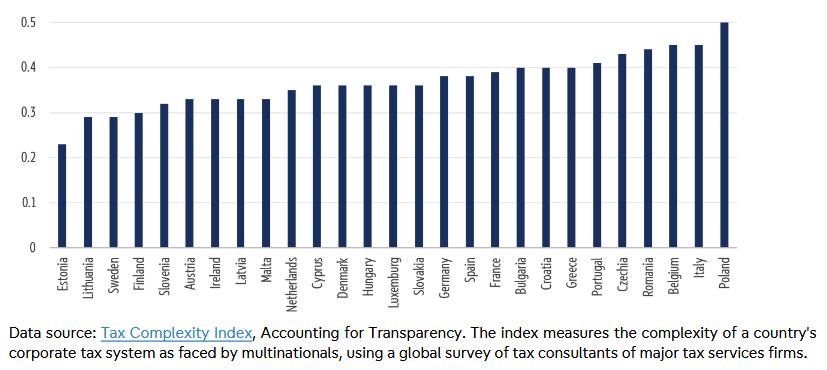

One European Commission study estimated that businesses within the EU-28 incurred on average an annual tax compliance cost equivalent to 1.9 % of their turnover in 2019. Moreover, these costs had more than doubled since 2014. Among the various taxes, businesses regarded value added tax (VAT) and corporate tax as those with the highest compliance burden, requiring the majority of smaller enterprises to outsource these tasks to specialised firms. Other studies have also criticised the way that the implementation of recent EU anti-tax abuse measures have come at the cost of a ‘complexity explosion’.

Lowering tax compliance costs is not a straightforward one-size-fits-all exercise. Compliance costs are unevenly distributed among firms, influenced by several factors. Younger companies often face higher compliance costs due to the learning curve they experience in meeting regulatory requirements. Smaller firms also tend to bear relatively higher costs compared to larger companies. Furthermore, sectors that benefit from multiple special tax rates or specific deductible items (for instance, the energy sector) often face more complex compliance efforts as a result. The performance of Member States also varies, with the Baltic and Nordic countries tending to have lower corporate tax compliance costs.

To rephrase the well-known saying, tax compliance costs are as certain in life as taxes themselves. While lowering compliance costs can be desirable, eliminating or reducing essential reporting requirements can hinder tax authorities’ ability to detect illegal or abusive tax practices. To build a tax system that guarantees both fairness and revenue generation, a certain level of administrative complexity is unavoidable, requiring policymakers to strike the right balance.

Simplifying taxation in the EU

While the precise legislative initiatives to be taken by the new Commissioner in charge of taxation are not yet known, the Commission’s taxation department recently held public consultations on the Anti-Tax-Avoidance Directive (ATAD) and the Directive on Administrative Cooperation (DAC). The results of these evaluations may feed into potential future proposals for revising both directives.

A shared concern among a number of stakeholders was ATAD’s fragmented implementation across the EU. The directive introduced a number of minimum standards for key measures aimed at curbing aggressive corporate tax planning, but left room for Member States to apply supplementary rules if they wished. While ‘gold-plating’ – the practice of adding extra requirements to EU regulations – can support domestic policy goals, it can also cause companies ‘additional and avoidable regulatory costs‘, Draghi warns. Letta advises prioritising the use of binding ‘regulations’ rather than directives to ensure a more harmonised implementation of EU law. In the area of tax, switching from directives – which are the usual approach – to regulations may be challenging. Since taxation remains a national competence, Member States may favour the flexibility of directives, which can, in turn, increase the chances of securing the unanimous support needed in the Council for the legislation’s adoption.

There are a number of legislative files pending in the Council that seek to lower the business tax regulatory burden, including those on VAT in the digital age, BEFIT, and HOT.

Further reading

- D’Andria D. and Heinemann M., Overview on the tax compliance costs faced by European enterprises – with a focus on SMEs, Policy Department for Economic, Scientific and Quality of Life Policies, European Parliament, 2023.

- Heckemeyer J., Removal of taxation-based obstacles and distortions in the Single Market in order to encourage cross border investment, Policy Department for Economic, Scientific and Quality of Life Policies, European Parliament, 2022.

- KPMG/VVA, Tax Compliance Costs for SMEs, 2022.

Read this ‘at a glance’ note on ‘Tax compliance costs in the EU: Striking the right balance‘ in the Think Tank pages of the European Parliament.

EP Think Tank paper: Tax compliance costs in the EU: Striking the right balance