Paris, 13 August 2024

Highlights

- Global oil demand increased by 870 kb/d in 2Q24, with a contraction in China limiting gains. Demand is set to rise by less than 1 mb/d in both 2024 and 2025. This is largely unchanged from last month’s Report and far slower than last year’s 2.1 mb/d growth as comparatively lacklustre macroeconomic drivers come to the fore.

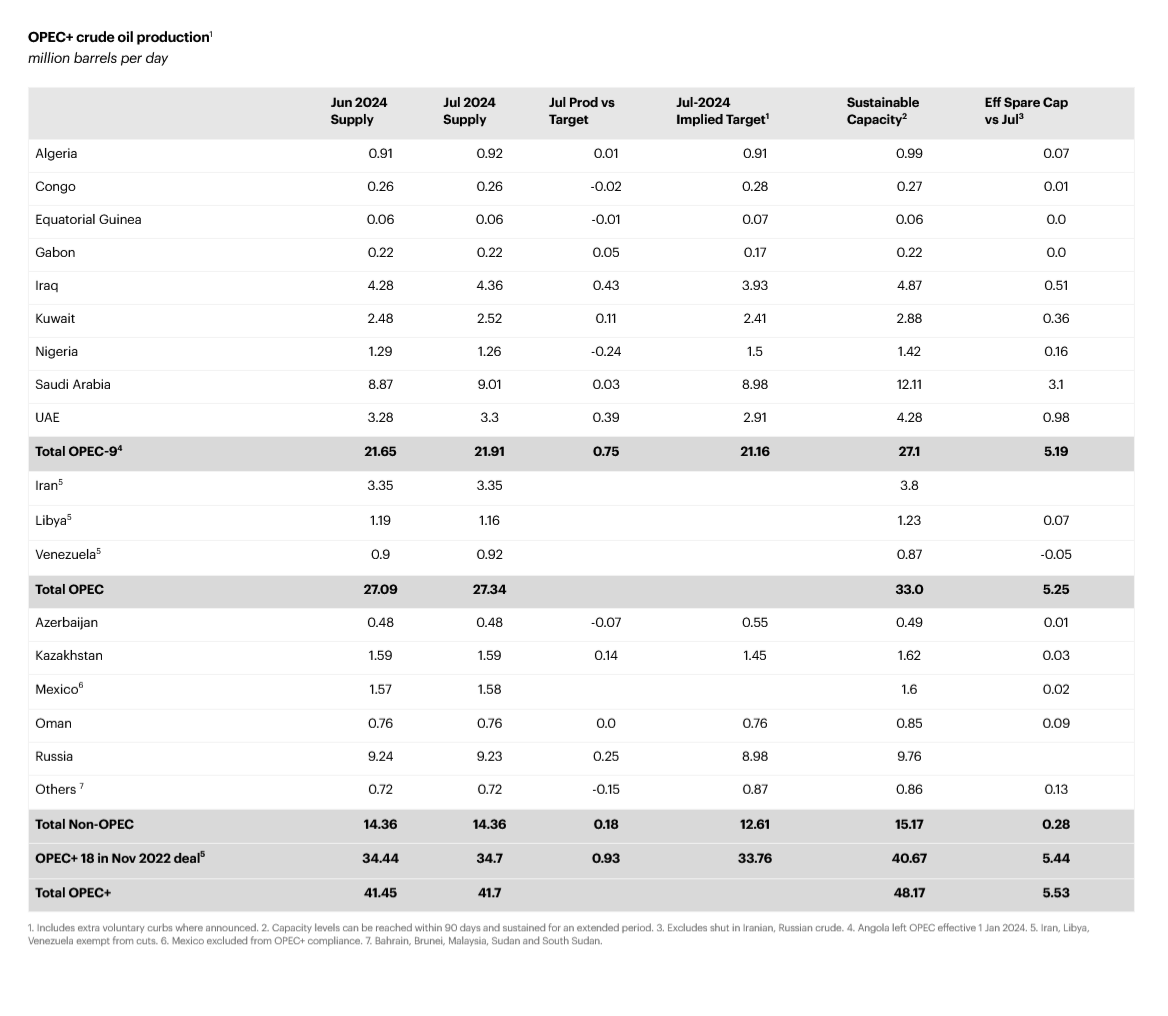

- World supply rose 230 kb/d to 103.4 mb/d in July as a substantial OPEC+ increase more than offset losses from non-OPEC+. Annual gains accelerate from 730 kb/d in 2024 to 1.9 mb/d in 2025. Non-OPEC+ production increases by 1.5 mb/d this year and next, while OPEC+ may fall by 760 kb/d in 2024 but rise by 400 kb/d in 2025 if voluntary cuts stay in place.

- Global refinery throughputs are forecast to increase by 840 kb/d to 83.3 mb/d in 2024, and by 600 kb/d to 83.9 mb/d next year. Margin weakness continues to weigh on processing rates, with Chinese runs now expected to decline y-o-y. Margins fell further in July in Europe, but rose in Singapore and on the US Gulf Coast, led by stronger naphtha and gasoline cracks.

- Global observed oil inventories fell by 26.2 mb in June, following four months of builds totalling 157.5 mb. OECD onshore stocks declined by 19.5 mb but were mostly offset by a 17.5 mb increase in non-OECD countries. Oil on water declined for a third consecutive month, by 24.2 mb. OECD Industry inventories were down by 21 mb, largely in line with the seasonal norm.

- Brent crude futures tumbled by $6/bbl during July, as a string of weak macro-economic data prompted a broad risk-off sentiment across financial markets, outweighing escalating hostilities in the Middle East. Front-month time spreads remained resilient in the face of falling flat prices, reflecting a tight Atlantic Basin market. At the time of writing, Brent was trading at around $80/bbl.

Market gymnastics

Oil markets exhibited Olympic levels of volatility over recent weeks. Benchmark crude oil prices tumbled sharply lower in July and early August as unexpected economic data threw the market off balance. Questions over the health of the global economy re-emerged as Japan increased interest rates sparking a reversal in yen carry trades, China’s outlook deteriorated and US hiring slowed in July. But persistent geopolitical tensions in the Middle East and some relatively positive macroeconomic data backstopped weakness in oil futures, with prices rebounding higher in the second week of August. Moreover, OPEC+ cuts are also tightening physical markets, lifting North Sea Dated to a $2/bbl premium against the front-month ICE contract. At the time of writing, ICE Brent futures traded at around $80/bbl, down by more than $6/bbl since the start of July.

Our outlook for global oil demand is largely unchanged from last month’s Report, with growth projected at slightly less than 1 mb/d in both 2024 and 2025. However, a meaningful shift in drivers is becoming apparent. In June, Chinese oil demand contracted for a third consecutive month, driven by a slump in industrial inputs, including for the petrochemical sector. Preliminary trade data point to further weakness in July, as crude oil imports sank to their lowest level since the stringent lockdowns of September 2022. By contrast, demand in advanced economies, especially for US gasoline, has shown signs of strength in recent months. The US economy, where one-third of global gasoline is consumed, has outperformed peers, with a resilient service sector buttressing miles driven. As a result, OECD oil consumption flipped from a 300 kb/d annual contraction in 1Q24 to growth of 190 kb/d in the second quarter.

Despite the marked slowdown in Chinese oil demand growth, OPEC+ has yet to call time on its plan to gradually unwind voluntary production cuts starting in the fourth quarter. Its Joint Ministerial Monitoring Committee (JMMC) reiterated on 1 August, however, that the group could pause or reverse its decision depending on prevailing market conditions. Our current balances suggest that even if those cuts remain in place, global inventories could build by an average 860 kb/d next year as non-OPEC+ supply increases of around 1.5 mb/d in 2024 and again in 2025 more than cover expected demand growth. The Americas quartet of the United States, Guyana, Canada and Brazil account for three-quarters, or roughly 1.1 mb/d, of non-OPEC+ supply gains in each of the two years.

For now, supply is struggling to keep pace with peak summer demand, tipping the market into a deficit. As a result, global inventories have taken a hit. After four months of gains, June saw oil inventories fall by 26.2 mb. Crude oil stocks dropped by 40.9 mb, even as China built substantially. Meanwhile, oil products rose by 14.8 mb, supported by large builds in US LPG. Preliminary July data suggest this trend continued, with total stocks declining once again as crude inventories lost further ground while oil products made gains. This dynamic is squeezing refinery margins, potentially setting the stage for an upset and shift in refinery activity in the coming months. Competition in the oil markets will continue even after the Olympic and Paralympic.

About this report

The IEA Oil Market Report (OMR) is one of the world’s most authoritative and timely sources of data, forecasts and analysis on the global oil market – including detailed statistics and commentary on oil supply, demand, inventories, prices and refining activity, as well as oil trade for IEA and selected non-IEA countries.

Source – IEA