Paris, 2 May 2024

Watch the live webcast of the press conference

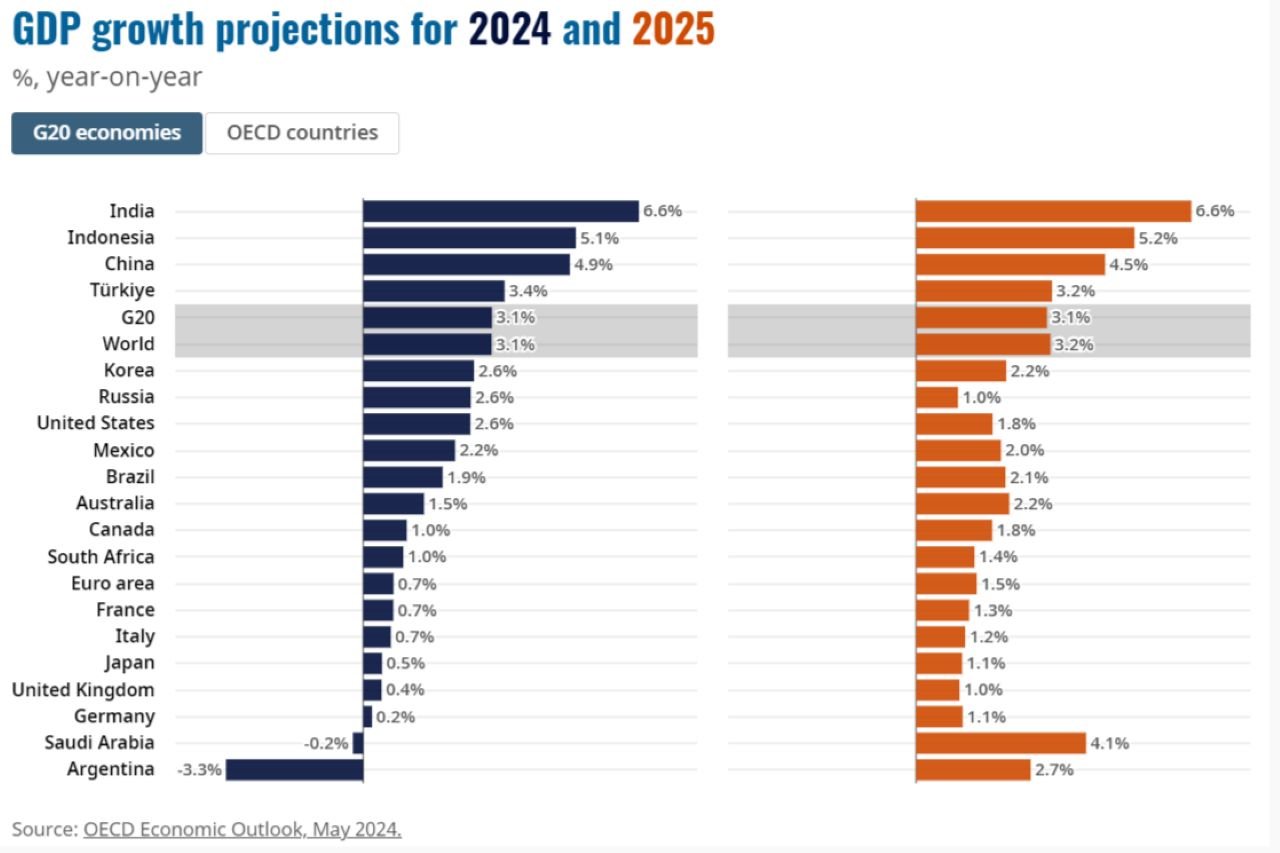

The global economy is continuing growing at a modest pace, according to the OECD’s latest Economic Outlook. The Economic Outlook projects steady global GDP growth of 3.1% in 2024, the same as the 3.1% in 2023, followed by a slight pick-up to 3.2% in 2025.

The impact of tight monetary conditions continues being felt, particularly in housing and credit markets, but global activity is proving relatively resilient, the decline in inflation continues, and private sector confidence is improving.

The OECD unemployment rate stood at 4.9% in February, close to its lowest levels since 2001. Real incomes are rising in many OECD countries as inflation moderates, and trade growth has turned positive. The outlook continues to differ across countries, with weaker outcomes in many advanced economies, especially in Europe, and strong growth in the United States and many emerging market economies.

Headline inflation in the OECD is projected to gradually ease from 6.9% in 2023 to 5.0% in 2024 and 3.4% in 2025, helped by tight monetary policy and fading goods and energy price pressures. By the end of 2025, inflation is expected to be back on central bank targets in most major economies.

GDP growth in the United States is projected to be 2.6% in 2024, before slowing to 1.8% in 2025 as the economy adapts to high borrowing costs and moderating domestic demand. In the euro area, which stagnated in the fourth quarter of 2023, a recovery in real household incomes, tight labour markets and reductions in policy interest rates will help generate a gradual rebound. Euro area GDP growth is projected at 0.7% in 2024 and 1.5% in 2025.

Growth in Japan should recover steadily, with domestic demand underpinned by stronger real wage growth, continued accommodative monetary policy and temporary tax cuts. GDP is projected to expand by 0.5% in 2024 and 1.1% in 2025.

China is expected to slow moderately, with GDP growth of 4.9% in 2024 and 4.5% in 2025, as the economy is supported by fiscal stimulus and exports.

“The global economy has proved resilient, inflation has declined within sight of central bank targets, and risks to the outlook are becoming more balanced. We expect steady global growth for 2024 and 2025, though growth is projected to remain below its longer-run average,” OECD Secretary-General Mathias Cormann said. “Policy action needs to ensure macroeconomic stability and improve medium-term growth prospects. Monetary policy should remain prudent, with scope to lower policy interest rates as inflation declines, fiscal policy needs to address rising pressures to debt sustainability, and policy reforms should boost innovation, investment and opportunities in the labour market particularly for women, young people and older workers.”

Significant uncertainty remains. Inflation may stay higher for longer, resulting in slower-than-expected reductions in policy interest rates and leading to further financial vulnerabilities. Growth could disappoint in China, due to the persistent weakness in property markets or smaller-than-anticipated fiscal support over the next two years. High geopolitical tensions remain a significant near-term risk to activity and inflation, particularly if the evolving conflict in the Middle East and attacks in the Red Sea were to widen or escalate. On the upside, demand growth could prove stronger than expected, if households and firms were to draw more fully on the savings accumulated during COVID-19.

Against this backdrop, the Outlook lays out a series of policy recommendations, highlighting the need to ensure a durable reduction in inflation, establish a budgetary path that will address rising fiscal pressures and undertake reforms that improve prospects for medium-term growth.

Monetary policy needs to remain prudent, to ensure that inflationary pressures are durably contained. Scope exists to lower policy interest rates as inflation declines, but the policy stance should remain restrictive in most major economies for some time to come.

Governments face rising fiscal challenges given high debt levels and sizeable additional spending pressures from population ageing, and climate adaptation and mitigation. Future debt burdens are likely to rise significantly if no action is taken, highlighting the need for stronger near-term efforts to contain spending growth, improve public spending efficiency, reallocate spending to areas that better support opportunities and growth, and optimise tax revenues.

“The foundations for future output and productivity growth need to be strengthened by ambitious structural policy reforms to improve human capital and take advantage of technological advances,” OECD Chief Economist Clare Lombardelli said.

For the full report and more information, visit the Economic Outlook online.

Working with over 100 countries, the OECD is a global policy forum that promotes policies to preserve individual liberty and improve the economic and social well-being of people around the world.

Source – OECD